Featured

Table of Contents

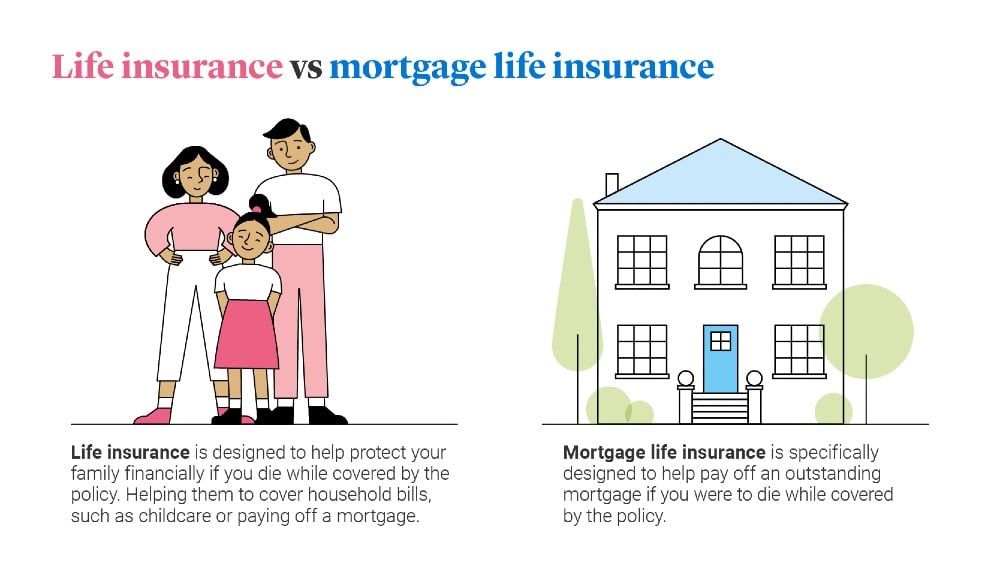

Here's how the two contrast. The essential distinction: MPI protection pays off the staying balance on your home mortgage, whereas life insurance provides your beneficiaries a fatality benefit that can be used for any function (life insurance to get a mortgage).

A lot of plans have an optimum limit on the dimension of the home mortgage balance that can be guaranteed. This maximum amount will be clarified when you get your Mortgage Life Insurance coverage, and will be recorded in your certification of insurance coverage. Also if your starting home loan equilibrium is higher than the optimum restriction, you can still guarantee it up to that restriction.

They also like the truth that the earnings of her mortgage life insurance policy will go straight to pay out the home loan balance instead than possibly being made use of to pay various other financial obligations. buying a house life insurance. It is necessary to Anne-Sophie that her family will have the ability to proceed living in their household home, without financial pressure

Keeping all of these phrases and insurance kinds straight can be a migraine. The adhering to table positions them side-by-side so you can promptly set apart among them if you obtain puzzled. One more insurance coverage kind that can repay your mortgage if you die is a standard life insurance coverage policy.

Insurance To Payoff Mortgage In Case Of Death

A is in area for an established number of years, such as 10, 20 or 30 years, and pays your beneficiaries if you were to pass away during that term. A gives coverage for your whole life span and pays out when you pass away.

One usual guideline is to aim for a life insurance policy policy that will pay out approximately 10 times the insurance holder's income amount. Alternatively, you could pick to use something like the DIME method, which adds a household's financial debt, income, mortgage and education and learning expenditures to compute exactly how much life insurance is required.

It's likewise worth noting that there are age-related restrictions and thresholds enforced by virtually all insurance providers, that commonly won't give older purchasers as several choices, will bill them much more or might deny them outright. mortgage insurance coverage requirements.

Home Insurance Loan

Here's just how home loan security insurance determines up against standard life insurance coverage. If you have the ability to qualify for term life insurance policy, you must stay clear of home loan security insurance policy (MPI). Compared to MPI, life insurance provides your household a less costly and extra flexible advantage that you can rely on. It'll pay out the exact same quantity no issue when in the term a death occurs, and the money can be made use of to cover any type of expenses your family members regards essential during that time.

In those situations, MPI can give excellent peace of mind. Every mortgage defense alternative will certainly have numerous regulations, regulations, advantage options and drawbacks that need to be evaluated very carefully against your specific scenario.

A life insurance policy plan can aid pay off your home's home loan if you were to pass away. It is just one of several methods that life insurance coverage might aid shield your liked ones and their financial future. Among the ideal methods to factor your mortgage into your life insurance coverage requirement is to chat with your insurance policy representative.

Rather than a one-size-fits-all life insurance plan, American Family members Life Insurance policy Company provides policies that can be designed specifically to satisfy your family's demands. Below are a few of your alternatives: A term life insurance coverage policy (insured mortgages) is active for a specific amount of time and typically supplies a larger quantity of protection at a reduced cost than a long-term plan

A whole life insurance policy plan is simply what it appears like. Rather than just covering an established number of years, it can cover you for your whole life. It also has living advantages, such as money worth buildup. * American Family Life Insurer supplies various life insurance policy policies. Talk with your agent concerning tailoring a plan or a combination of policies today and getting the comfort you deserve.

Your agent is a great source to address your concerns. They may likewise have the ability to aid you locate voids in your life insurance policy coverage or new methods to minimize your other insurance plan. ***Yes. A life insurance policy beneficiary can pick to use the fatality advantage for anything. It's an excellent means to aid protect the financial future of your household if you were to pass away.

Life Insurance For Mortgages Quotes

Life insurance policy is one way of aiding your family members in paying off a home loan if you were to pass away prior to the home loan is entirely paid off. Life insurance coverage profits may be used to aid pay off a home loan, but it is not the exact same as mortgage insurance coverage that you might be required to have as a problem of a financing.

Life insurance policy might aid guarantee your home stays in your family members by giving a death advantage that may assist pay down a mortgage or make vital acquisitions if you were to pass away. This is a brief summary of coverage and is subject to plan and/or biker terms and problems, which might vary by state - cheap loan insurance.

What Is The Difference Between Mortgage Insurance And Homeowners Insurance

The words life time, long-lasting and irreversible undergo plan conditions. * Any type of fundings extracted from your life insurance coverage policy will build up interest. Any type of outstanding finance balance (finance plus rate of interest) will be deducted from the fatality advantage at the time of insurance claim or from the cash value at the time of surrender.

Discount rates do not apply to the life plan. Policy Kinds: ICC18-33 (10 ), ICC18-33 (15 ), ICC18-34 (20 ), ICC18-35 (30 ), L-33 (10 )(ND), L-33 (15 )(ND), L-34 (20 )(ND), L-35 (30 )(ND), L-33 (10 )(SD), L-33 (15 )(SD), L-34 (20 )(SD), L-35 (30 )(SD), ICC18-36 (10 ), ICC18-36 (15 ), ICC18-36 (20 ), ICC18-36 (30 ), L-36 (10 )(ND), L-36 (15 )(ND), L-36 (20 )(ND), L-36 (30 )(ND), L-36 (10 )(SD), L-36 (15 )(SD), L-36 (20 )(SD), L-36 (30 )(SD), ICC17-225 WL, L-225 (ND) WL, L-225 WL, ICC17-227 WL, L-227 (ND) WL, L-227 WL, ICC17-223 WL, L-223 (ND) WL, L-223 WL, ICC17-224 WL, L-224 (ND) WL, L-224 WL, ICC17-228 WL, L-228 (ND) WL, L-228 WL, ICC21, L141, MS 01 22, L141, ND 02 22, L141, SD 02 22 - standard life mortgage ppi.

Home loan security insurance (MPI) is a different kind of safeguard that could be useful if you're not able to settle your home mortgage. While that extra defense sounds good, MPI isn't for every person. Below's when mortgage security insurance coverage deserves it. Home loan protection insurance coverage is an insurance coverage that repays the rest of your home mortgage if you die or if you end up being handicapped and can't work.

Like PMI, MIP shields the loan provider, not you. Unlike PMI, you'll pay MIP for the duration of the financing term. Both PMI and MIP are needed insurance coverage coverages. An MPI policy is completely optional. The quantity you'll pay for home loan protection insurance coverage relies on a variety of aspects, including the insurance firm and the current balance of your mortgage.

Still, there are advantages and disadvantages: Most MPI plans are provided on a "guaranteed acceptance" basis. That can be advantageous if you have a health problem and pay high rates forever insurance policy or struggle to get coverage. An MPI plan can offer you and your family members with a sense of safety.

Mortgage Protection Plan Reviews

You can select whether you require mortgage security insurance and for how long you need it. You might desire your home mortgage security insurance coverage term to be close in size to how long you have actually left to pay off your home mortgage You can cancel a home loan defense insurance coverage plan.

{kind=link}

Latest Posts

Burial Insurance Over 80

What Is Funeral Cover

Instant Term Life Insurance Coverage